If the taxpayer has doubts about the legality of the actions or requirements of the tax inspector who conducted the "camera room", he has the right to draw up an objection to the act of the cameral tax audit, a sample of which is presented below. How to draw up and in what case should not be submitted? We will try to give a detailed answer to each question.

Reasons for filing an objection

Tax inspectors, having received the taxpayer's declaration and other documents on income / expenses, conduct a desk audit of these business papers. In the event that any information requires clarification or clarification, the payer is notified accordingly. Within the time limits established by law, he is obliged to provide all Required documents, references, etc. Identified violations become the basis for drawing up an act of the inspection, which is sent to the person being checked.

If an entrepreneur (head of an organization) decides that his rights were violated during the audit, he has the right to file an objection to the act of a cameral tax audit.

The reasons for its compilation are conventionally divided by experts into two categories:

- procedural violations (violated the rules of the "camera meeting");

- substantive law violations (the inspector misinterpreted any papers, did not take into account all the documents that the payer provided).

There are violations that are not recognized as serious, and an attempt to point them out can turn against the taxpayer. Do not focus on the following shortcomings of the inspector:

- timing of the “cameral meeting” (beginning and end);

- minor inaccuracies in the preparation of the act;

- non-serious violations of the rules.

The document must be submitted to the tax office in person or sent by mail. In the latter case, it is advisable to send it by registered mail with notice. Alternatively, you can use the Internet. However, this option is only suitable for those who have a digital signature (officially registered).

Compilation features

Before drawing up an objection, it is recommended to make sure that the fact of violations by the inspectors really took place, and that there are no pitfalls and errors in the activities of the entrepreneur. Otherwise, another (repeated) check may reveal serious violations in the activities of the entrepreneur himself.

The document must be submitted on paper, because:

- only in this form will it be accepted by a higher tax authority;

- it may be needed when going to court.

All formulations must be clear, and the argument must be one hundred percent. Otherwise, legally savvy state. employees will be able to quickly “destroy” an incorrectly drafted charge of the taxpayer.

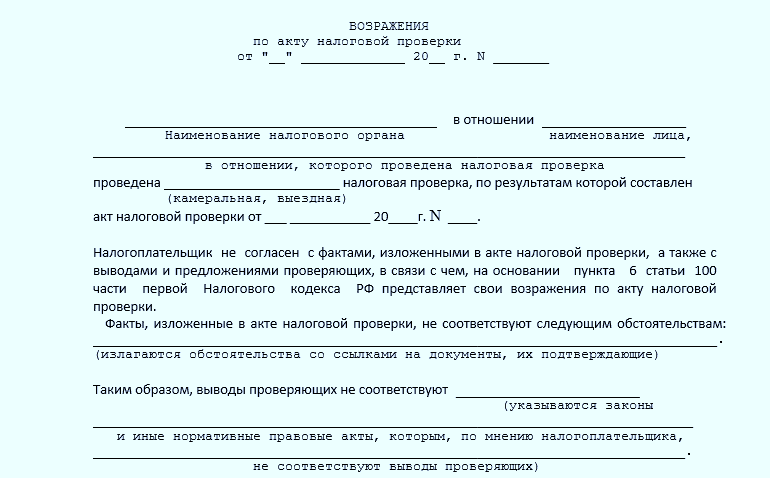

Sample document

To date, there is no clearly defined form of objection. Even on the official website of the Federal Tax Service, an approximate example is given. However, the logic and rules of office work suggest what and how to indicate:

- at the beginning of the document (upper right corner) - information about the addressee (name of the tax organization, name, surname and position of the tax inspector who conducted the desk audit);

- further - information about the sender (taxpayer);

- then - the number of the document and the date of its compilation.

In the main body of the document you should write its name (“Objection to the act ...”) and provide your evidence of the violations identified. It is recommended to refer to the articles tax code, Letters of the Ministry of Finance and other regulations.

In the final part, the payer must summarize, indicate his request (requirements). If any documents are attached to the objection, their list should be given in the "Appendix" section. The document must be signed by an official (head of the company). It is necessary to indicate his position, last name, first name and put the date.

At the legislative level, it is not spelled out how to draw up an objection to the act of "camera house". This means that you can fill in by hand ready-made form or print on a computer using text editor and then print on a printer using a regular A4 sheet or company letterhead. It is also not necessary to put a company seal. This rule was abolished in 2016.

The objection is made in two copies. One taxpayer keeps for himself after the tax inspector approves him. Gives another copy to the tax office.

State. employees are required to notify the taxpayer of the date, time and place of his objections. He may be present and supplement his claims with new arguments or apply for a reduction in the fine, since there are extenuating circumstances (in this case, the amount should be halved). However, his presence is not necessary, this will not aggravate the situation.

So, the objection to the act of a desk audit is a document that is drawn up by the taxpayer. The reason for the compilation is the actions of the inspector who conducted the check, which, in the opinion of the payer, violated the legislative norms and the rights of the person being checked. There are no strict requirements for its design, but it is desirable to draw it up if there are good reasons.

The act at the end of the audit and the procedure for appealing it

Act of tax audit in accordance with Art. 100 tax code Russian Federation(hereinafter - TC) is a document drawn up by a representative of the regulatory authority upon completion of this procedure. The need and time for preparation depends on the type of audit:

- during an on-site inspection, the act is drawn up in any case, no later than 2 months from the date of drawing up a certificate of the inspection carried out (in relation to the consolidated group - 3 months);

- cameral - only in the presence of violations, within 10 days after its completion.

It should be noted that an act is not yet a decision to hold or not to hold liable. The person in respect of whom the audit was carried out has the right to influence its results by submitting objections to the above document (clause 1, article 21, clause 6, article 100 of the Tax Code).

IMPORTANT! An appeal against the act of a tax audit is made within a month from the date of its receipt. For a consolidated group of persons, such period is 30 days from the date of receipt.

By virtue of Art. 101 of the Tax Code act, other documents containing information about violations, objections are considered by the head of the IFTS within 10 days from the date of the deadline for submitting objections in accordance with paragraph 6 of Art. 100 NK.

How to make objections: an example

It is recommended that you familiarize yourself with an example of a sample of objections to a tax audit report after studying the procedure for its execution below.

The document is drawn up in writing. The law does not provide for any special requirements for its content, therefore, registration in any form is acceptable. Usually, when describing their position, references are made to the provisions of legislative acts and clarifications of state bodies, as well as judicial practice.

As attachments to the letter, you should indicate the documents that are evidence confirming the stated arguments. They can be submitted before the decision is made, even after the submission of the application.

The order of compilation is as follows:

- The name of the body that carried out the control measures and its address, the name of the taxpayer, his address and telephone number are indicated in the upper right part of the document.

- Title: name, number and date of the document under appeal.

- The main part: what violations were identified and why the author does not agree with them.

- Pleading part: a specific request is expressed, for example, for VAT deductibility.

- Signature of the authorized person, transcript of the signature (full name, position), date of signing.

Arguments to answer in a VAT dispute

When filing objections to a VAT tax audit report, the following can be used as arguments:

- If the basis for non-acceptance for deduction is the failure to exercise due diligence when choosing a counterparty, evidence of a proper verification of the partner’s good faith should be provided (for example, the decision of the Arbitration Court of the Ural District dated December 21, 2015 No. F09-9048 / 15 in case No. A76-4061 / 2015).

- When the deduction is not made due to the fact that the counterparty is on the simplified tax system, you can refer to the right granted to the seller, who is on the simplified tax system, by law (subparagraph 1, clause 5, article 173 of the Tax Code) to issue an invoice to the buyer with VAT and pay it to the budget (for example, Decree of the Federal Antimonopoly Service of the Moscow District of May 28, 2007, June 1, 2007 No. KA-A40 / 3414-07 in case No. A40-69643 / 06-99-332). In the sample response to the act of tax audit, presented in this article, you can get acquainted with this justification in more detail.

- In case of refusal to refund VAT on the basis of non-return of advance payments, prove the legitimacy of applying the deduction calculated from the received advance (for example, Resolution of the Federal Antimonopoly Service of the Moscow District dated April 21, 2010 No. KA-A40 / 3418-10 in case No. 40-91717 / 09-129-567 ).

What you need to consider when filing an appeal against an act

When starting the procedure for appealing the conclusions of the IFTS, the following rules established by law should be borne in mind:

- The decision made before the end of the period for challenging the act will be canceled if the taxpayer was not notified of the date of consideration of the audit materials (clause 14 of article 101 of the Tax Code).

- The absence of a written statement of disagreement with the results of the audit does not exclude the possibility of giving explanations in the process of considering its materials (clause 4, article 101 of the Tax Code).

- An appeal may entail the need for additional tax control measures (clause 6, article 101 of the Tax Code). At the same time, the period for consideration of materials and making a final decision may be extended, but not more than for 1 month.

- If the deadline for filing written objections to the tax audit report and making a decision is missed, all that remains is to appeal the decision to a higher tax authority or court (subparagraph 12, paragraph 1, article 21, article 137, subparagraphs 1, 2, article 138 of the Tax Code).

An act drawn up based on the results of an inspection by a representative of a controlling body can be challenged by submitting a corresponding written application addressed to the head of the same body. This must be done within the time period established by law, clearly and reasonably stating your position. Evidence confirming the validity of the application can be submitted both simultaneously with it and after (before the decision is made).

After the tax audit, the organization receives an act on its results within the prescribed period. In case of disagreement with the content of the act, the taxpayer has the right to submit reasoned objections. Objections are an expression of disagreement with the findings of the audit with reference to the official legislative framework. Written objections are accompanied by oral explanations, the provision of the necessary documents.

As a result, the decision may be canceled tax office in whole or in a separate part based on the results of cameral and on-site inspections. It is very important to build the right strategy. Due to the complexity of this task, it can only be solved in a team. You will need the help of a tax consultant, a lawyer. The participation of an anti-crisis and arbitration manager, an auditor is optimal.

Appeal steps

It is permissible to express claims and objections within a certain period of time after familiarization with the inspection report. They must be sent to the tax authority (superior), in the absence of the desired result, go to court.

Obtaining an act of the performed check

According to the results of the control (on-site or cameral), an act should be drawn up indicating the facts of violations found with the signature of the inspector. Two months are given for this from the period of issuing a certificate of a completed tax audit. And according to the results of the cameral control, only 10 days are allotted for this procedure if violations in the calculation of fees (taxes) are detected. In the absence of such, the act is not relevant at all.

Within five calendar days, the act must be handed over to the subject of verification. If he refuses to receive it, then this is noted in the act, which is sent by registered mail. The time of its delivery is supposed to be considered the sixth day from the date of departure. The taxpayer has the right not to sign the act, but this indirectly may raise suspicions of his dishonesty. In addition, signing it does not mean unconditional agreement with the conclusions.

The taxpayer may disagree with the act by presenting his objections. In this case, he can use the right to provide the tax authority with his explanations and disagreement with the results. Motivated objections must be submitted within a month. The beginning of such a period is considered to be following the delivery this act day.

IMPORTANT: Already at the stage of delivery of the act, it is necessary to pay attention in order to track possible procedural violations on the part of the inspectors. This can help in the future in asserting their rights. After all, serious violations already at this stage can serve as a reason for the cancellation (full or partial) of the decision of the tax commission.

The alleged errors in the act may be as follows:

- arithmetic - errors in calculations; as a result - inaccurate calculation of accrued fines and penalties;

- erroneous assessment of documents, facts;

- misjudgment of business transactions.

Many errors in the procedure of inspection work can be eliminated even in the process of studying the results of the inspection. Additional measures for this purpose may be initiated by the head of the inspectorate. Therefore, it is not recommended to voice the main claims at this time. It is better to use them during the period when the final decision on the act is made, by contacting the instance of a higher authority or the court.

Violations of tax control can conditionally be differentiated into two groups: procedural, material (incorrect interpretation of the regulations). If there are objections to the procedural actions, it is possible to decide on additional control measures, and this is risky.

Pre-trial appeal procedure

Or - filing objections to a higher authority. By different types tax audits, a procedure for pre-trial resolution of tax disputes has been developed. A person has the right to go to court upon completion of an attempt to resolve the issue in a higher authority. Before you decide to appeal the results, you need to seriously weigh everything, to understand the essence of your claims.

Development sequence

- careful study of the submitted act of the audit;

- singling out points on which there are disagreements;

- drawing up the actual objections to the content of the act or to certain parts of it in a free form.

Objections must be submitted in writing in free form. To disagree with the conclusions, the verified subject has the right to cast doubt on the entire act or on one of its parts, both the facts and the conclusions. Objections may be formulated on the merits or on procedural issues.

Objections must be submitted in writing in free form. To disagree with the conclusions, the verified subject has the right to cast doubt on the entire act or on one of its parts, both the facts and the conclusions. Objections may be formulated on the merits or on procedural issues.

It is recommended to cite sections of the act with which there is no agreement in order. The position should be voiced clearly, convincingly arguing, based on the legislative norms that were in force during the verification period (after all, they can change). Use examples of legal proceedings, making reference to them. There are two ways to file objections: in person to the tax authority or by mail.

Rules for filing claims with a higher authority

- file objections in writing;

- use clear, coherent reasoning;

- substantiate each objection;

- present evidence using copies of documents;

- provide after the arguments references to the regulatory framework;

- strictly comply with the deadlines established by law;

- send the documents to the inspectorate that carried out the inspection.

Based on the results of studying the objections, the head of the inspection must make a decision. Its options may be as follows:

- Bring to justice the persons who have committed a tax offense.

- Refuse to hold the said persons accountable for not confirming the facts.

Why you should be on the committee

It is not necessary to do this. However, it definitely can't hurt. In addition, with personal presence there are opportunities:

- add oral comments, arguments to written requirements;

- provide additional documentation;

- waive objections, but cite mitigating circumstances in order to reduce the amount of penalties.

Action after an objection

After a pre-trial appeal against the conclusions of tax control bodies (objections), the inspectorate is obliged to make an appropriate decision. According to the audit, a higher authority holds the tax organization liable for the alleged offense or refuses to do so.

Involved tax organizations receive information about the decision, which reflects:

- the circumstances of the violation;

- the grounds and documents that made it possible to draw such a conclusion;

- decision on the possibility of bringing to responsibility in accordance with a certain article of the Tax Code of the Russian Federation;

- the financial size of the discovered arrears.

Initiation of a claim with a package of objections to the court

The higher tax organization often confirms the decision of the lower organization. To challenge the results, the organization has the right to apply to the court within three months. This method of challenging is considered more effective, although not easy. Often the motivation of taxpayers is recognized as formal. Therefore, it is necessary to carefully collect evidence of relationships with counterparties, the economic feasibility of transactions.

Drafting a document

When compiling a document, the following rules must be observed:

At the end of the document, a similar text usually follows: “We believe that the proposed conclusions are not a reflection of the actual state of affairs, they are in conflict with the tax legislation on such grounds…” Reasonable arguments follow. And in conclusion, note: “Taking into account our justifications, supported by the attached documents, we insist on the cancellation of the act of the tax audit (or certain points thereof) and before the accrual of tax amounts (indicate specific amounts).”

Application Design Rules

- Documents used to help substantiate objections may be attached. They can be transferred to the inspection and separately.

- Each copy of a single page document is certified separately (and not as a binder).

- Multi-page documents are certified by one signature, regardless of the number of pages. However, the sheets must be bound and numbered.

Form of possible objection

It is allowed to file objections in any form. It is important that all points of the act that caused disagreement be listed, the reasons for disagreement are justified, links to documents are attached. The document requires the signature of the head, the presence of the seal of the organization.

Objections must be drawn up in two copies (the first for inspection, the other is stored in the organization). When sending a document by mail, you must receive a notification of its receipt.

Sample parts of the document

General or introductory part. In another way, it is called the information component of the check. This part should contain the following points:

- indication of the exact details of the person being checked;

- indication of the time of presentation (proposal) of objections;

- time characteristics of the check;

- direction of control measures.

- an indication of the specific parts of the inspection report that caused disagreement;

- substantiation of the submitted objections with references to the official legislative framework;

- analysis of the arbitration practice that has developed in the region in the area under consideration.

Resolution part. The final part contains the following information:

- Total amount of objections, total. Claims of the objecting person, request for the cancellation of the verification act.

You can find an example objection form at the link below:

IMPORTANT: Justifying your own position on the issue under consideration, you need to take into account the norms of the Tax Code of the Russian Federation, explanations of the Federal Tax Service and the Ministry of Finance of the Russian Federation.

Submission procedure

- Weigh your decision and the essence of the claims, once again check all the disagreements with the tax legislation.

- State all objections to the act or to some of its clauses in writing using a special form.

- Submit written reasoned objections to the appropriate inspection.

- To substantiate the objections, attach the necessary documents (copies).

Peculiarities of consideration of available verification materials

When considering the submitted audit materials, each taxpayer or his representative is granted the right to be present. But this is optional. Presentation during the meeting additional documents to existing written objections is allowed. Additional requirements, additions will be recorded in the protocol. They will be accepted and studied.

The commission is obliged to hand over the version of the protocol. If a person is present at the meeting without written objections, they can always be expressed orally. At the commission, you can also refuse the written objections presented earlier.

If the objections are insignificant, it makes sense to apply for a reduction in the amount of penalties in connection with the taxpayer's extenuating circumstances to reduce the fine. By visiting the commission, you can achieve at least a minimal improvement in the state of affairs, so it is recommended to do this.

Terms of consideration

An act based on the results of the audit is formed in two months (three months for a consolidated group), even if no violations are detected. Another five days are given for handing it to the official with the attached documents (ten in the case of a group). In the case of sending a document by mail, its delivery is dated the sixth day from the date of sending.

The deadline for filing reasonable objections to the act in writing of the audit carried out is measured according to the Tax Code of the Russian Federation as one month from the period of receipt of the act (from next day or from the seventh day if received by registered mail).

The head of the auditing tax authority considers objections within ten days. It begins at the end of the period provided for the submission of claims, regardless of when they were actually filed. Extension of the term is possible, but not longer than a month.

The place and period of consideration of the results of control must be known to the taxpayer. He has the right to take part in the consideration of the submitted materials. Making a decision before the expiration of the prescribed month is considered a violation of the procedure for consideration.

Objections can help the company: cancel or reduce penalties. But it is important to take into account all the pros and cons, because as a result, complications in the preparation of the results of the audit, additional measures, and examination are possible.

Living and dead water: myth or reality, what is the power of living and dead water?

Craniosynostosis, or premature fusion of the bones of the skull Frontal crest in a child

Beautiful hair How to achieve hair density at home: useful tips

Why mosquitoes bite some people, but not others

How to achieve beautiful hair