An individual entrepreneur (IP), or, as it used to be called, a private entrepreneur, is an individual who has the registration of an entrepreneur without forming a legal entity, but in fact owns many of the rights of legal entities. The rules of the civil code apply to individual entrepreneurs (IP).

Whatever system of taxation an individual entrepreneur is on, he still undertakes to make regular contributions to the Pension Fund. An individual entrepreneur can find out all the necessary data on his own at a branch of the Pension Fund or wait until the amount of the mandatory payment is calculated and all the data is sent for making the payment.

Payment of insurance premiums

There are situations when an individual entrepreneur, due to certain circumstances, does not stop its activities, but does not receive income. In this case, the law stipulates the possibility of non-payment of insurance premiums. These periods include:

- time spent in the army on conscription;

- the time when a small child is cared for by the time he reaches 1.5 years;

- caring for a disabled person of group I, a disabled child or a person who has reached the age of 80;

- in the case of living with a spouse who serves under a contract;

- for the period of temporary stay with the spouse abroad, in connection with sending him abroad from the place of work.

A prerequisite for the temporary termination of payments in connection with the above circumstances is the availability of documents that will confirm them.

To date, there are two categories of IP in terms of the amount of earnings per year:

- Individual entrepreneurs earning less than 300 thousand rubles a year.

- Individual entrepreneurs whose income is more than 300 thousand rubles a year.

After separation according to this principle, individual entrepreneurs are considered unequal in their obligations for payments to the Pension Fund. An individual entrepreneur of the first category is obliged to pay a fixed rate to the Pension Fund. Today, this amount is 23,153.33 rubles a year, or, if we talk about a monthly payment, then 1,929.44 rubles.

Distribution by funds:

- in the Pension Fund of the Russian Federation: 19,356.48 rubles. + 1%;

- in FFOMS: 3,796.85 rubles.

As for the second category of individual entrepreneurs, they make two mandatory contributions to the Pension Fund of Russia. The first payment includes a mandatory deduction provided for all entrepreneurs. The second mandatory payment is 1 percent of the amount that exceeded the bar of 300 thousand rubles.

Dependence of income and taxation system:

- for the simplified tax system, all income is taken, which is taken into account when calculating the tax;

- for the Unified tax on imputed income, the imputed income for the year is taken;

- if the patent system is calculated on the estimated income from which the patent value was calculated.

How is 1% calculated?

Let's take an example of how 1 percent is calculated on the amount of income over three hundred thousand rubles.

Suppose that for the reporting year, the IP earned 700,000 rubles. Regardless of the amount of income, he will pay 23,153.33 rubles as an entrepreneur of the first category. In addition, you will additionally have to pay 1 percent of 400 thousand rubles (700,000 - 300,000 = 400,000), and in monetary terms it will look like this: 400,000 × 1% (0.01) = 4,000 rubles.

Thus, the total amount of the mandatory payment to the Pension Fund is 27,153.33 rubles.

It would seem that 1 percent is a very small and insignificant rate, but at the same time it will bring a rather significant increase in revenues to the state budget. Despite the fact that the government decided to introduce it, it also took care to establish an upper limit for taxation. Even with a very high annual income, the maximum 1% rate cannot exceed the amount of 158,648.69 rubles.

The object of taxation should also be noted, because the regimes can be different and their incomes are calculated differently. That is why it was decided that income, both in the OSNO and in the simplified taxation system, is taken in its pure form, not taking into account the amount of expenses (we remind you that the USN system provides for “income minus expenses” of 15%). If an individual entrepreneur applies several taxation regimes, then for the correctness of the calculations, it is necessary to sum up all incomes.

How are Pension Fund contributions paid?

For individual entrepreneurs who are on the general taxation system, and those that use the simplified system, the amount of expenses is not taken into account when calculating income for paying insurance premiums.

Insurance premiums in the presence of an incomplete year

If you registered as an individual entrepreneur some time after the year began, then, of course, you will pay less insurance premiums.

And in order to accurately calculate it and avoid any errors, you can use a special formula. It consists of the sum of the products of the fixed contribution rate per month (in the Pension Fund of the Russian Federation - 19,356.48 rubles + 1%, in the FFOMS - 3,796.85 rubles), multiplied by the number of full months in a year from the date of registration, and the same rate , multiplied by the number of calendar days in the status of an individual entrepreneur (of that incomplete month when registration was carried out), divided by the total number of calendar days of an incomplete month:

SV = FV × M + FV × D1 ÷ D2

An individual entrepreneur has the right to pay all the debt for the year in a single lump sum, and then he is obliged to meet the payment by December 31 of the year for which payment is made.

Most often, contributions are paid once a quarter, since then the individual entrepreneur also gets the opportunity to reduce the tax to the Federal Tax Service by the amount of these same paid insurance premiums. For example, an individual entrepreneur who does not have employees has the right to reduce the amount of taxes to be paid by one hundred percent of insurance premiums. An individual entrepreneur who has employees - by 50%.

By the end of the year, the individual entrepreneur has the opportunity to evaluate the income received for the analyzed period and calculate the amount of the mandatory payment to the Pension Fund as an additional insurance premium. The transfer must be made before April 1 of the next year after the reporting year.

Since 2012, a big bonus for individual entrepreneurs has been the fact that they no longer need to submit reports directly to the Pension Fund, but just submit another income declaration to the tax office. Further, the authorities will sort it out among themselves on their own, but a report must be submitted to the Federal Tax Service, since in the absence of data, the Pension Fund must recover pension insurance premiums from the violator, based on the maximum tariff.

To pay insurance premiums, three different payments are used: in the PFR - for a fixed part and an additional 1%, as well as in the FFOMS.

- 392 1 02 02140 06 1100 160 - CSC for a fixed contribution to the PFR;

- 392 1 02 02103 08 1011 160 - CSC for the established contribution to the FFOMS;

- 392 1 02 02140 06 1200 160 - CCC for transferring an additional 1% to the PFR.

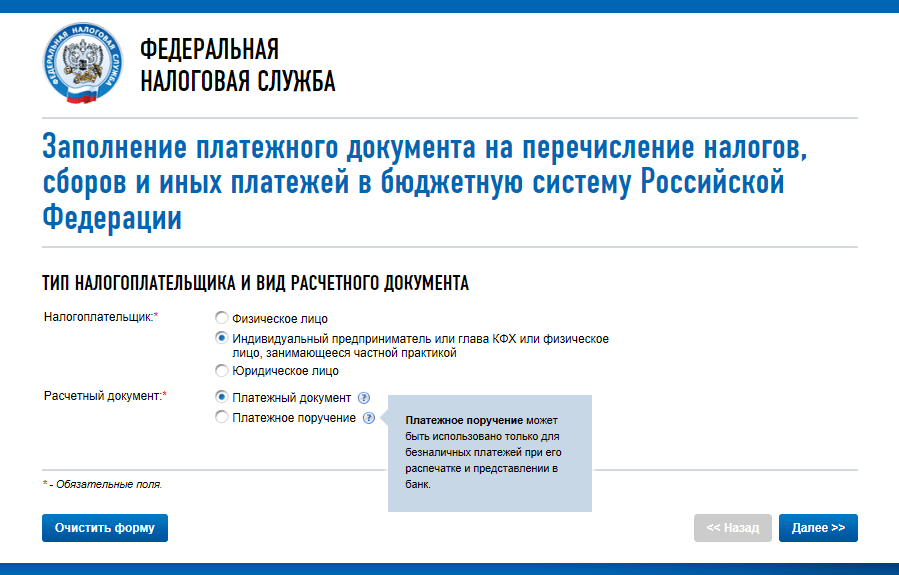

An example of filling out a payment order for the payment of insurance premiums

Payer status (field 101): 08.

Payer (field 8): last name, first name and patronymic (SP) //address of residence//. For example, Tinkova Olga Yurievna (IP) //740521, Sverdlovsk, st. Polevaya, 11, apt. 73//

Order of payment (field 21): 6

Code (field 22): 0.

Payer checkpoint (field 102): 0.

BCC (field 104): according to the contribution.

OKTMO (field 105): your OKTMO code.

In fields 106-110: 0.

Purpose of payment (field 24):

The registration number in the FIU is 087-000-000000. Insurance contributions to the PFR in a fixed amount for the insurance part of the pension (from the amount of income not exceeding 300 thousand rubles) for 2019 - for fixed contributions to the PFR.

The registration number in the FIU is 087-000-000000. Insurance contributions to the Pension Fund in a fixed amount for the insurance part of the pension (from the amount of income over 300 thousand rubles) for 2019 - for an additional 1 percent to the Pension Fund.

The registration number in the FIU is 087-000-000000. Insurance contributions for CHI to the FFOMS budget for 2019 - for fixed contributions to the FFOMS.

If, as a result of checking your reports, you find that you have transferred either an erroneous amount or an amount exceeding the required payment, then you have the opportunity to contact the Pension Fund assigned to your territory and submit a written application for the offset (refund) of these payments to within 3 years from the date of payment of the specified amount.

If, in the event of an error, an overpayment of insurance premiums was made, then the possibility of offsetting from one off-budget fund to another (from the PFR to the MHIF and vice versa) against the following payments is legally prescribed.

Entrepreneurs conducting their business on preferential taxation systems independently, without resorting to hiring employees, pay contributions to the Pension Fund (PFR) and the Compulsory Medical Insurance Fund (FOMS). Due to the conflicting actions of the Ministry of Finance, businessmen confused the budget classification codes (BCC) for different periods of payment of 1% over 300,000 rubles. for IP in PF in 2018. Why this situation has developed and to what budget to transfer money for 2017 and 2018, read in the article.

Initially, the Ministry of Finance, in Order No. 255n, approved in December 2017, proposed to split the payment of fixed pension contributions. To transfer contributions from income not exceeding 300 thousand rubles a year, one CCC was used, and for payments from the remaining amount, another. Thus, if an entrepreneur received less than 300 thousand rubles for the billing period, then he used one KBK. If the revenue exceeded this value, then the money had to be transferred using two different codes. That is, the BCC for insurance premiums to the Pension Fund for 2018 "for oneself" from amounts over 300,000 rubles. different from the base. Additional payments were transferred to a specially created account, which took into account contributions of 1% over the limit of 300,000 rubles.

Despite the fact that the order was approved in December 2017, its publication took place only in February 2018. However, the Ministry of Finance quickly realized that such a division was not economically feasible and created additional difficulties for accountants. At the end of February of this year, a new order No. 35n was drawn up, canceling the division of the KBK. The legal act was published on April 23 and entered into force on May 3.

Therefore, the BCC for IP contributions of 1 percent to the Pension Fund for 2017-2018. in the current year is identical to the code for fixed contributions from income not exceeding 300 thousand rubles:

18210202140061110160

The transfer of fixed contributions to the PFR is carried out within the following terms (paragraph 2, part 2, article 432 of the Tax Code of the Russian Federation):

- until December 31, 2017, the fixed contribution itself is paid, until July 2, 2018 - 1% of income above the established limit for the past 2017;

- until January 9, 2019 the main contribution, until July 1, 2019 - 1% of the profit over the limit for 2018.

If the entrepreneur made a payment from income over 300 thousand rubles. at 1% for BCC for individual entrepreneurs in 2018, approved by order No. 255n

18210202140061210160,

it is recommended to write an application for clarification to the local branch of the FIU. Otherwise, even the funds transferred in good faith may not be taken into account in state bodies, and a fine or penalties will be charged to the name of the entrepreneur.

Table of sizes of fixed IP contributions in 2018-2019

CCC for fixed IP contributions in 2018-2019

From what amount is 1% calculated for IP on the simplified tax system 15% and on the OSNO?

Knowing the BCC for individual entrepreneurs to transfer 1 percent to the Pension Fund for 2018, it is necessary to correctly calculate the amount of additional contributions. Some individual entrepreneurs on the simplified tax system of 15% (“income minus expenses”) with a base rate or a general taxation system (OSNO) still literally interpret the provisions of the Tax Code (TC) of the Russian Federation. They calculate the amount of payment from income in excess of 300 thousand per year, excluding expenses.

This approach, indeed, was applied until 2017. But since last year, entrepreneurs have been allowed to pay 1% to the Pension Fund only from the difference between profit and costs. Additional clarification to Art. 210 and paragraph 1, part 9 of Art. 430 NC was given by the Ministry of Finance. Letter No. 03-15-07/8369, published by the Ministry of Finance in February 2018, states that it is necessary to take into account the specifics of preferential regimes. For example, with a simplified tax system of 6% (“income”), UTII and a patent, all income is taken into account without deducting expenses. For OSNO and STS, 15% tax base is determined as the difference between profit and costs. you can test the service for free, which will do everything for you.

An individual entrepreneur can transfer to the FIU according to the current CCC 1% of income over 300,000 rubles. in any quarter, while the payment deadlines for 2018 will be met. Thus, the payment can be divided into several parts, reducing the total amount of tax payments.

Calculation examples of 1% additional contribution to the PFR for different taxation regimes

Example No. 1: IP Petrov I.Yu. operates on USN 6%. In 2018, he received 950 thousand rubles. income.

In order to find out what amount Petrov I.Yew. is obliged to pay to the FIU, he will need to use the formula:

(SD - 300,000) * 0.01,

where SD is the amount of income for the billing period.

We carry out calculations:

(950,000 - 300,000) * 0.01 \u003d 650,000 * 0.01 \u003d 6,500 rubles.

We calculate the total amount of insurance payable to the FIU:

26,545 + 6,500 = 33,045 rubles

The entrepreneur can pay up to January 9, 2019 the entire amount with interest immediately. Or he can first pay a fixed contribution, and by July 1, 2019, transfer 1% of more than 300,000 rubles through the CCC to the PFR. for IP income in 2018.

Example No. 2: IP Ignatieva A.F. acquired a patent for the provision of services in a photo studio in the amount of 360 thousand rubles. The period of validity of a patent certificate is 12 months. For the year Ignatieva A.F. received a profit of 450 thousand rubles.

Some accountants may decide that Ignatieva A.F. must make additional contributions from the actual income received. However, for the patent system (PSN) only the amount spent on the acquisition of the certificate matters. Real profit will not be taken into account.

(360 000 – 300 000) * 0,01 = 60 000 * 0,01 = 600

The total amount of payment to the Pension Fund will be:

26,545 + 600 = 27,145 rubles

Example No. 3: IP Mamontov R.S. conducts business using UTII. According to calculations, his annual profit amounted to 780 thousand rubles. Income in each quarter was the same: 195 thousand rubles. Mamontov R.S. paid an additional tax of 1 percent of turnover in 2018 from the II to the IV quarter.

As mentioned above, additional contributions may be paid in quarterly installments. But here it is important not to get confused in the calculations.

Calculate profit for the second quarter:

195 000 * 2 = 390 000

We do the calculation:

(390 000 – 300 000) * 0,01 = 90 000 * 0,01 = 900

To calculate the fixed payments of an individual entrepreneur in 2017, a minimum wage equal to 7,500 rubles is applied. per month.

Thus, the cost of an insurance year in a fixed amount for compulsory health insurance is 4590.00 rub.(Minimum wage x 5.1% x 12). It is necessary to pay insurance premiums for the FFOMS before January 9, 2018 (December 31, 2017 is a day off).

Please note that insurance contributions to the FFOMS from January 1, 2017 are administered by the tax service. Therefore, insurance premiums must be transferred to the account of the Federal Tax Service at the place of residence of the individual entrepreneur. BCC for transferring insurance premiums for individual entrepreneurs to the FFOMS 18210202103081013160.

Insurance premiums in a fixed amount for 2017 for mandatory pension insurance.

Until January 9, 2018 (December 31, 2017 day off), individual entrepreneurs and heads of peasant farms and members of peasant farms must pay fixed insurance premiums in the amount of 23,400 ru. (7500 rubles * 26% * 12 months).

Please note that from January 1, 2017, insurance contributions to the FIU are administered by the tax service. Therefore, insurance premiums must be transferred to the account of the Federal Tax Service at the place of residence of the individual entrepreneur. 18210202140061110160.

Those individual entrepreneurs who received income in 2017 with more than 300,000 rubles. must pay to the IFTS additional fixed insurance premiums in the amount of 1% of revenue, but not more than 187,200 rubles. taking into account a fixed payment paid before December 31, 2017 (RUB 23,400). Such a payment must be paid to the IFTS no later than July 2, 2018. BCC for transferring insurance premiums for individual entrepreneurs to the FIU 18210202140061110160.

From April 23, new CBCs are in effect for IP contributions

The calculation of the fixed payment is made according to the formula:

(IP income - 300,000 rubles) * 1%.

Those. if in 2017 the income of an individual entrepreneur is 10,000,000 rubles, then the amount of a fixed payment to the FIU will be 97,000 rubles. ((10,000,000 - 300,000)*1%). The total amount of fiused insurance premiums to the Pension Fund for 2017 of this individual entrepreneur will be 120,400 rubles. (23400 +97 000).

If the IP income for 2017 is RUB 19,020,000 and more, then the amount of fixed insurance premiums in the Pension Fund for 2017 will be 187,200 rubles. ((19,020,000 -300,000)*1%), which the IP must pay until January 9, 2018(December 31, 2017 day off) in the amount of 23,400 rubles. and before July 2, 2018 in the amount of 163,800 rubles.

We recommend that an individual entrepreneur on a "roshchenka" pay fixed insurance premiums for 2017 to the Federal Tax Service by December 31, 2017. In this case, the tax on the contributions paid can be reduced to 100% or the contributions can be taken into account in expenses.

The amount of insurance premiums for the billing period is determined in proportion to the number of calendar months, starting from the month of commencement (end) of activity. For an incomplete month of activity, the amount of insurance premiums is determined in proportion to the number of calendar days of this month.

FOR 2017

|

IP with an income of up to 300 thousand rubles. in year, Heads of KFH and members of KFH |

IP with an income of over 300 thousand rubles. in year |

|

1 minimum wage * 26% * 12 CONTRIBUTION TO PFR = 23400.00 rubles. |

1 minimum wage * 26% * 12 + 1.0% of the amount> 300 thousand rubles. Max.: 8MRO*26%*12 = RUB 187,200.00 CONTRIBUTION TO PFR = RUB 23,400.00+ + (INCOME-300000)*1% until July 2, 2018 - 1% of income. |

The amount of insurance premiums for 2018-2020

The amount of insurance premiums for 2018-2020

Since 2018, the procedure for calculating fixed contributions for individual entrepreneurs, lawyers, heads and members of peasant farms, etc. has been changed. Article 430 of the Tax Code of the Russian Federation provides for the values \u200b\u200bof fixed contributions that do not depend on the minimum wage, as in 2015-2017.

Contributions to the PFR from income exceeding 300,000 rubles. will be calculated as 1% of the excess amount, but not more than the maximum allowable value.

Fixed IP contributions for 2018-2020

| Insurance contributions to the PFR, FFOMS |

2018 |

2019 year |

2020 |

|---|---|---|---|

|

Mandatory contribution to the PFR from income not exceeding 300,000 rubles. |

RUB 26,545 |

RUB 29,354 |

RUB 32,448 |

|

The maximum allowable amount of contributions to the FIU |

RUB 212,360 (RUB 26,545 ×8) |

RUB 234,832 (RUB 29,354 ×8) |

RUB 259,584 (RUB 32,448 ×8) |

|

Contributions to the MHIF |

5 840 rub. |

RUB 6,884 |

RUB 8,426 |

The deadline for paying "pension" contributions from income exceeding 300,000 rubles. starting from the reporting for 2017, it is necessary to pay no later than July 1 of the following year for the reporting year.

So for 2017, insurance premiums to the PFR from the excess amount must be paid no later than July 2, 2018 (since July 1, 2018 is a day off).

Insurance premiums for the heads of peasant farms and their members are also fixed and correspond to the minimum amount of insurance premiums in the PFR and FFOMS.

Some CBCs indicated by entrepreneurs when transferring taxes and insurance premiums are the same for all individual entrepreneurs, regardless of the applicable taxation regime. And some budget classification codes are “intended” for a specific regime.

CCC: IP-2019 contributions

CBCs for insurance premiums represent the largest group of codes that are necessary for entrepreneurs of absolutely all taxation regimes.

Individual entrepreneurs, when filling out payments for insurance premiums in 2019, must indicate the following BCC:

| Contribution type | KBK |

|---|---|

| Insurance premiums for OPS | 182 1 02 02010 06 1010 160 |

| Insurance premiums for CHI | 182 1 02 02101 08 1013 160 |

| Insurance premiums for VNiM | 182 1 02 02090 07 1010 160 |

| Injury insurance premiums | 393 1 02 02050 07 1000 160 |

| Additional insurance premiums for compulsory pension insurance for employees who work in conditions that give the right to early retirement, including: | |

| 182 1 02 02131 06 1010 160 | |

| - for those employed in jobs with harmful working conditions (clause 1, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ | 182 1 02 02131 06 1020 160 |

| ) (additional tariff does not depend on the results of the special assessment) | 182 1 02 02132 06 1010 160 |

| - for those employed in jobs with difficult working conditions (clauses 2-18, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (additional tariff depends on the results of the special assessment) | 182 1 02 02132 06 1020 160 |

KBC: IP contributions for yourself

BCCs for IP contributions for themselves are also the same for everyone, regardless of the applied regime.

BCC for IP on DOS in 2019

General business entrepreneurs are payers of personal income tax in part of their income and payers of VAT:

BCC for individual entrepreneurs in special modes in 2019

Each special regime tax has its own CSC.

It has long been noted that pension contributions are one of the most serious financial burdens on microbusiness. Often it exceeds even the standard tax. Starting from 2017, when the administration of insurance premiums from two off-budget funds was transferred to the hands of the Federal Tax Service of the Russian Federation, these fiscal fees by entrepreneurs began to be included in taxes in everyday life. At the same time, pension contributions are recognized as the most serious burden placed on small businesses. Consider what other contributions there are and the features of their payment, including if the income of an individual entrepreneur exceeds 300 thousand rubles.

Pension and other insurance premiums

For all private entrepreneurs working alone, and for those who have hired employees, a number of mandatory insurance payments have been established, which include:

- Payments for pension and medical insurance (OPS and CHI):

- the amount of a fixed payment for a pension is set by the Government of the Russian Federation for 2018 in the amount of 26,545 ₽;

- the insurance premium for CHI is 5,840 ₽;

- in total, every year until December 31, each merchant registered in the unified register, where all entrepreneurs of the Russian Federation are entered, is obliged to pay a fee in the amount of 32,385 ₽ to the state insurance treasury;

- these mandatory amounts are annually indexed based on inflation and the economic situation in the country. To date, exact figures have been determined for the period up to 2021;

- the amount of the insurance fee imputed to all individual entrepreneurs is not tied to the profit of a commercial micro-enterprise. For the tax regulator, the figure of IP income is absolutely not important here. The controller is not interested in the fact whether the business worked or the activity was not carried out. In this matter, all private entrepreneurs are equal in responsibilities;

- benefits are not provided to anyone, the amount of the fixed payment is the same for everyone. At a superficial glance, the logic is not visible, but both individual entrepreneurs who are already on a well-deserved pension and working citizens (until they retain the status of an entrepreneur) pay mandatory insurance premiums. If you are registered with the USRIP - pay the insurance fee without fail.

- The percentage of all payments to their employees (for individual entrepreneurs who, respectively, have them), and not only for the OPS and CHI, but also the mandatory social tax in the FSS (in case the employees of the IP receive a disability certificate). In this case, the contribution to compensation in case of illness of the entrepreneur himself is considered voluntary. Accordingly, if a merchant does not pay a contribution to the FSS, then he is not entitled to compensation for sick leave.

- And the last mandatory insurance contribution, which goes strictly to the pension piggy bank, is 1% of the total business income in excess of 300,000 rubles. Moreover, this fee is paid regardless of the payment of a fixed fee (clause 1).

And we note that when control over payments for all insurance premiums (with the exception of social insurance payments to the FSS) passes to the tax authority, regulation in terms and forms becomes more and more stringent. This is noted by all working IP. It is more difficult to negotiate with the tax authorities than it was when communicating with funds, control over settlements is carried out more carefully, and violations are punished immediately.

Payment of IP turnover tax exceeding 300 thousand per year: terms, procedure, formula and calculation example

So, the payment in excess of business profits of three hundred thousand rubles or more is calculated based on the percentage of the total IP turnover. The collection rate is set at one percent of the amount exceeding 300,000 ₽. The calculation is based on the total figure for the calendar year.

And you should pay attention: if a businessman works under two or more tax regimes, then the income from each of the taxation systems in the aggregate will be taken into account.

An example of a calculation when combining a simplified tax base with a 6% tax base and a single imputed tax (UTII):

The first initial amount is the gross profit under the simplified IP regime, which amounted to 290,000 rubles for the reporting period;

The second revenue part, which will be taken into account in the calculation of turnover, is the UTII tax charge imputed to the entrepreneur. Take, for example, 200,000 rubles for a full calendar year.

Accordingly, we consider the total turnover of individual entrepreneurs under two tax regimes: 290,000 ₽ + 200,000 ₽ = 490,000 ₽.

The calculation of the insurance fee in this case will look like this: 490,000 ₽ (total income) - 300,000 ₽ (income limit) = 190,000 ₽ (the amount subject to insurance premium) / 100 (or multiply by 1%) = 1,900 rubles.

Thus, in order to calculate the payment for the mandatory pension tax, it is necessary to subtract 300 thousand from the amount of profit for all taxation systems used by individual entrepreneurs, and divide the total by a coefficient equal to one hundred units. This will be the figure that the business must pay for pension insurance if the business limit is exceeded.

What incomes to take into account when calculating 1% for OPS, depending on the IP mode

So, there are usually no difficulties in calculating the amount of payment of one percent of a turnover of more than 300 thousand rubles. Questions begin with determining the revenue side that should be taken into account when calculating this fee.

Here it is necessary to understand that the annual turnover of a businessman, subject to a fee of 1%, is calculated based on the tax base of the individual entrepreneur. In general, everything that is considered income when declaring is taken into account in the calculation of the insurance premium. And in the case of an imputation or a patent, this will be, respectively, the UTII tax imputed to the entrepreneur or the fee for permission under the PSN.

Understanding the details, it should be noted that when calculating the turnover of an individual entrepreneur, one must rely on legislative acts that apply under various tax regimes:

- IP income on the general basic IP regime is taken into account on the basis of the personal income tax declaration. That is, the calculation in excess of the OSNO contribution includes the profit of the individual entrepreneur minus business costs (this is established by section 210 of the Tax Code of the Russian Federation and the Resolution of the Constitutional Court of the Russian Federation No. 27-P).

- Individual entrepreneurs applying the simplified regime with the “income” tax base take into account all their gross profit (see Article 346.15 of the Code). Everything that has passed through the current account or cash desk of the business is taken into account in the calculation of the IP turnover.

- Entrepreneurs who work on the object "income - expenses" take into account only the income recorded in the declaration under the simplified tax system. Therefore, all business expenses are removed from the total volume.

- Agricultural producers using the UAT, which, by the way, since 2017 include outsourcing companies that assist farmers in caring for animals, harvesting crops, etc., take into account their business expenses when calculating the income.

- As already mentioned, individual entrepreneurs working on imputation take as a basis the amount of the tax fee imputed to them.

- Business on a patent (as well as IP on UTII) takes into account the full price of the purchased patent.

In tax and insurance accounting of the income part, the business should, first of all, be guided by the Book of Accounting for the Economic Activities of the IP. Recall that all entrepreneurs maintain this tax reporting document, regardless of the taxation system they use. And when summing up the results of entrepreneurial activity in the reporting period, the main beacon is just KUDiR. Each regime has its own, its own form and accounting operations. But the focal point - the profitable part - is always taken into account in the first place.

Note: there is no reporting of any IP insurance premiums that are paid “for themselves”. Here the regulator makes business a kind of indulgence. But do not hope that the tax controller does not monitor the turnover of microbusiness. This is done easily, as mentioned above, all income is checked against the declarations of entrepreneurs. Therefore, the tax authorities always keep their finger on the pulse and know whether private business should pay something to the state pension fund.

When calculating a contribution of 1% of income in excess of 300 thousand rubles, KUDiR and the IP declaration are taken as the basis

The maximum amount of payment under the OPS

An important condition for the payers of this pension fee is that for a business whose annual profit exceeds a certain amount for the reporting year, the maximum amount of the insurance payment under the OPS is set. So, in 2018, companies with a turnover of more than 21 million 240 thousand rubles were included in the highly profitable business that pays the maximum amount of the pension. Therefore, if the total net profit of an individual entrepreneur is approximately 1.8 million rubles per month, it makes no sense to calculate the pension over/contribution. You just need to pay the max figure of the insurance fee for the OPS. Just keep in mind that, as with fixed contributions, this fee is indexed every year, so the amount of the maximum payment by year will be equal to:

- 2018 - 212 360 ₽;

- 2019 - 234 832 ₽;

- 2020 - 259 584 ₽.

How to pay 1% when the turnover is exceeded: term, methods, how to generate a receipt, CSC for OPS

The main thing that has changed when paying a pension contribution when the limit of 300 thousand rubles is exceeded is that all insurance premiums have changed (with the exception of disability contributions to the Social Insurance Fund). Therefore, the key point when paying the pension over-contribution should be noted - the correct budget classification code (BCC) should be indicated. Since when transferring according to the old (valid until 2017) CBC, the money will not go to the tax authorities, accordingly, penalties and sanctions may be applied to the payer.

But let's not nightmare a start-up business: at least back in 2017, the tax authorities, together with the Treasury of the Russian Federation, manually corrected the mistakes of payers when insurance premiums were incorrectly transferred. Also today there is a certain form of application for a change in the BCC when crediting taxes and fees, but mistakes made when making payments lead to loss of time and unnecessary running around the authorities.

The second innovation on pension payments - since 2018, the deadline for paying in excess of the contribution has been postponed from the end of April to July 1. This step made the approach to calculating this fee more logical and, to some extent, insured entrepreneurs against mistakes. After all, when the deadline is postponed for 2 months, the individual entrepreneur undergoes a declaration, a desk audit, and, based on the data verified by the Federal Tax Service Inspectorate, pays an insurance premium.

It is quite simple to prepare a payment document for paying a pension if the limit established by law is exceeded; you can generate a receipt in any way convenient for an individual entrepreneur:

- It is allowed to make a payment using a client bank of any credit institution where the individual entrepreneur has a current account. For this case, Internet banking has ready-made payment forms. One example of this method is the Sberbank-Online service. There are such forms in young mobile Internet ba

- If there is no r / account, the best (and pay attention - free) way to generate a payment receipt for a business can be to fill out an order remotely on the Internet portal of the Federal Tax Service of the Russian Federation:

- on this online resource, you can enter all the necessary data into the payment, send it for printing and pay the fee for the OPS using the terminal through the bank's cash desk;

- you can also fill out a document and make an online payment using a bank card, via an electronic wallet or even via a pay-payment from a cell phone.

How to prepare a payment and pay a fee on the tax service portal

Let's try to understand the stages of generating a payment document on the tax service portal. Let's go through a few steps that will allow the payer to quickly make a payment for the OPS contribution, for this you need:

- Open a hyperlink to the page of the portal nalog.ru and proceed to the formation of a payment receipt. To do this, on the first tab, you need to select the type of payer - an individual entrepreneur, and also determine how the ticket will be paid:

- Next, you need to select the type of payment. We enter the required BCC without spaces - 18210202140061110160. In general, other details may not be needed, but if suddenly the payer does not know the code, additional (optional) tabs will help clarify the CCC. The name of the payment and its type will help you find the form you need.

To determine the type of payment, it is enough to enter the required CCC

- The choice of your tax office passes through the drop-down list. Quite simply, this can be done by filling out a block that makes it possible to determine the IFTS at the address of registration of the IP.

You can find "your" IFTS at the IP registration address

- Next, we enter the details of the payment: the rationale for the paragraph, the period for which the fee is paid. And the last - the amount of the collection.

Details of the payment document are selected depending on the contribution, there are drop-down lists everywhere

- We put down brief information on the payer: TIN and full name are enough. entrepreneur, let's move on.

It is mandatory to fill in the details of the IP-payer

- The next online payment section is just for clarifying the information entered.

We check everything and click on "pay"

- Choose the form of payment - cash or bank transfer.

Choose the form of payment for the payment document

- The receipt has been generated. It remains only to pay. In what way - the payer chooses. If the payment goes through the bank's cash desk, you can print a receipt.

- If the individual entrepreneur is ready to pay the contribution online from a bank card, on the page "Pay a payment document" you need to select a partner bank and transfer the pension fee. The money will go directly to the account of the tax authorities. If the credit institution in which the IP-payer has a r / account is not in the provided list, you can make a payment through the public services website (the first icon in the logos). From this resource, you can pay with a card of any bank and with the help of other services, for example, from an electronic wallet.

On the "Pay a payment document" page, select a partner bank and pay the pension fee

Video instruction: payment of contributions to the PFR through Sberbank-Online

Pay attention to one more thing about insurance and payments: when deregistering a business from the USRIP, an entrepreneur is given 15 days to pay all mandatory contributions, this list also includes a contribution established when the threshold of total turnover is exceeded.

How to reflect the accrual of 1% of IP income in accounting

Despite the fact that all individual entrepreneurs are not required to keep accounting records (this is enshrined in paragraph 2 of Article 6 of the Federal Law No. 402 “On Accounting”), an individual entrepreneur can keep his own accounting for additional financial control. One of the most convenient ways for this is the 1C Accounting 8 Program in edition 3.0. This accounting resource makes it possible to create pension postings using a routine operation under the code D 91.02 K 69.06.5.

In our case, all pension contributions of individual entrepreneurs, and as mentioned above, both contributions: both a fixed one and an excess contribution go to regulators for one purpose and CCC, are also reflected in the accounting. postings on one account - 69.06.5.

For information: contributions for fixed medical insurance of individual entrepreneurs go to account 69.06.3.

In the 1C online service, there is no need to make any special settings to display accruals and payments for the excess pension fee (as well as for other contributions). The main task is to make the posting on the correct account in 1C.

When transferring a pension payment for excess to the state budget, it is also necessary to correctly draw up the document “Debit from the current account”.

If an individual entrepreneur works according to the general basic regime (OSNO) or a simplified one with the object “income taking into account expenses”, the amount of accrued insurance premiums is fixed automatically in accounting for business costs.

Video: accounting entries when calculating IP insurance premiums in 1C Accounting 8

Few entrepreneurs know about the pension contribution paid when the income side is exceeded. But this is wrong. After all, every entrepreneur strives to develop his business and increase his income. In this case, knowing the full tax burden that can be charged to an individual entrepreneur is the right decision for a private growing company. Competent control of your business turnover and knowledge of the law will help in this.

How to understand: will the kitten be fluffy?

What kind of light alcohol can be drunk for pregnant women: the consequences of drinking

Why do the legs swell in the ankles and ankles of the feet in pregnant women: causes and methods of treatment

The wedding of Prince Harry and Meghan Markle: scandalous and secret details of the marriage (photo) The future marriage of Prince Harry year NTV

How to close white plums for the winter